Understand The Risk Management Or Pay The Price Later

71: The importance of understanding risk.

Welcome reader! It took us over 70 posts to write about maximizing efficiency and ensuring you are in a better position than those around you. It would only be fair if it took us 40 more to write the guide on positioning yourself and understanding. Better said, to give you an overview of risk management and how to approach it. Prepare yourself… This is a long post that everyone can benefit from.

Risk And Why It Matters

Why would you care? Risk is a topic that will start to make sense after you get out of "survival mode." When you are in a position to have time to think about what you want to get more out of your life instead of living paycheck to paycheck - once you stop being satisfied with the minimum. Since most of our readers are not living paycheck to paycheck and are out of survival mode. It is essential to understand what risk management is all about. People think they are in a unique situation (human nature) and purposely avoid reading things such as this one. That is not true. However, if you had a side business making 6 figures one year and the next year you are in 4 digits or that same business doesn't exist anymore… we can all agree that you took a series of wrong steps. You didn’t take the risk presented seriously enough. The same logic can be applied to investments, careers, and relationships. It is impossible to stay on top without experiencing pullbacks - no one can deny it. But experiencing drastic pullbacks and going from "hero to zero" should not be something you want. Solution? Risk management.

Making things easier for us: To get our point across, we split the readers into 4 categories based on their total assets. As with topics like this one, it is hard to give a single answer that fits all. We are sure there are outliers in this case as well, but that is something we cannot cover, and most readers of this post will fit into one of these groups. We did not consider age, as it would complicate things. Net worth is more than a good-enough metric and should help everyone understand where we are going with this.

1) Learning to avoid disaster - Mostly young people with $0 assets to their name. Yet to set themselves up with a predictable income (career), invest, or start a side business.

2) Living comfortably - Those with over $300k in assets and a predictable income have a high chance of running a side business and investing in stocks and crypto. Some may still have a debt that is managed with minimal effort.

3) Impossible to lose - Anyone with over $1-1.5 million, no debt and investments, predictable income, and a side business. All those from previous categories.

4) Not worth bothering with - If you are here, there is a good chance you have already hired someone to take care of your risks while focusing on other things. Congrats.

This doesn’t mean you should not follow the principles of the other groups. Let's say you are in group 1 and can invest in a stock you know will 3x. The choice is easy. The game is about playing all the fields and moving up. It is never linear or black and white.

Important to mention

We would argue this is still one of the best takes from legendary WSP regarding RE.

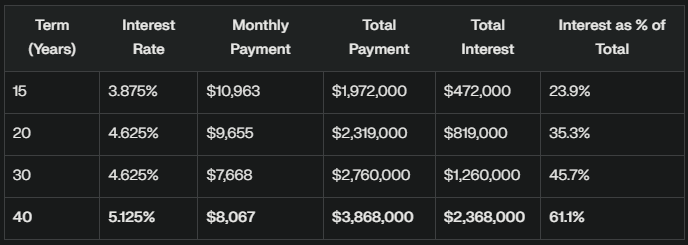

Real Estate: One of those topics we stay away from for a good reason. Over the last year, we have spoken with several people (mainly from Europe and the US) who have reported that their housing expenses have increased. This can mean only two things: living expenses (rent, bills) have increased, or their income has decreased. The second one is rarely the correct answer. We all know what has been happening for the last couple of years with everything else, not just real estate. This leaves you with the WSP approach and how to look at it. We don’t recommend getting into a long-term mortgage (debt) just to buy a place. If you are 100% sure that buying living space is right for you, ensure you have enough cash to minimize interest and not waste unnecessary money. Owning a place does not necessarily mean it will improve your life. If you haven't been in a good position before purchasing, it will decrease your quality of life - a common case. Before anyone comments, "Real estate prices always go up" that is not necessarily true. We leave this one up to you to decide what is worth it. Our last piece of advice regarding real estate? Avoid buying or getting into unnecessary debt before entering the last category. If you don’t believe us, look at yourself in the table below.

Example of a house costing $1.5 million and what you are looking at if you set yourself up for a 40-year plan. More than 2x the original price… Avoid.

Debt: Another topic we don’t want to touch in detail, as there are too many specific cases, and it is impossible to give proper advice without knowing the background. Neither is our goal to turn this post into a personal finance one. A big difference exists between having student debt at 2% interest and a car payment at 8%. One way to look at the debt and how to minimize the risk is from the outperforming perspective as long as you outperform the debt with your investments. You are good at paying the minimum - this way, you minimize the risk, as you know you will always be able to cover the debt. This approach is fine as long as you can get more out of your investment on the other side. It is better said that there is not much to worry about if you are in low digits up to 1-3%, and things get tricky when discussing higher single-digit numbers 6%+. To make things more practical. Let’s say your investment portfolio earns 7% per year after inflation. Your interest on the debt payment is 4%. This means you would be better off investing your money and paying the minimum debt as you go - the inflow of money is higher than the outflow. That is all the science there is on debt. Unfortunately, most do not invest in the first place, so they do not beat the debt anyway. Result? The majority realize they are better off paying off their debt.

Steps To Minimizing Risk

Minimizing risk: a long-term winning framework for those starting from zero.

Get predictable income (high-paying career)

Make sure you have at least 3 to 6 months of savings in case things go south

Start investing your money in a side business to get it off the ground (multiple income streams should be your goal)

Any money left after taking care of the side business → invest in stocks/crypto

Focus on building multiple income streams

Exit once side business income exceeds predictable income - when you are in a comfortable enough position

Learning To Avoid Disaster - Basics ($0 To Your Name)

Reality check: We have all been there. What separates those who make it from those who don’t? A strategy that revolves around minimizing risk-maximizing odds.

Living expenses: There is a reason why we are putting this first on the list. If you don’t have at least 3 to 6 months (depending on your position) of monthly expenses saved… You are doing something wrong. Not just wrong. Dangerous - something we have discussed multiple times on this website. If you are exposed to a risk that directly impacts your basics, you make short-term decisions. The short-term decisions? They lead to long-term losses. It is one big loop. One that once you notice, you won't be able to unnotice. This is boomer-type advice worth listening to. The minimum you want is not to worry about a roof over your head or to afford a healthy diet.

Predictable income (W2-career): If you have nothing going on and are without any cash flow. Starting the business or trying to hit it big could be a mistake. To start a business, you need money. Suppose you want to drive traffic to sell the products you are offering. You need money. Working for someone else in the same industry for 2 years while trying to start your side business? Underrated. It is one of those things that don’t get as much attention. That is the proper way to find mentors and exponentially speed up your learning process. Since we want to avoid getting away from the main idea of this post - keep it simple. What you should do is aim for a high-paying career in a growing industry, such as tech. This will allow you multiple options and ensure you are in a favorable position that brings you enough money. This advice is no longer popular, and there is a good reason… Most careers are not worth it. But if you follow our advice and know what you are doing, there is not much to worry about. All it takes is a few years of effort in your early life that will set you up for the future.

Side business: Essential piece of the puzzle. Side business. Why? Because the side business will bring you more than anything else regarding scalability. This means that all the money you have left from your predictable income after you take care of your basic needs should go into a side business. Luckily, 80% of the online side business can be started for less than $150 - which no one thought was possible years ago. Meaning? You have one less excuse not to start. You want to understand basics such as those presented in practical advice for business owners and start as soon as possible. The bigger problem is the sacrifices you must make along the way. The first few years are brutal, and you should put in maximum effort to get things off the ground. Remember that all the money you have left after covering your expenses should be prioritized for starting your business.

Company - pension match: This should be self-explanatory. Whenever you are presented with the opportunity to receive an employer contribution - pension match on your investment. You already know what to do… We won’t discuss any specifics, as each country has a different approach. Overall, the system works on the same principles. You put $100 into the S&P 500, and your company or pension fund does the same. Without a doubt, it has the lowest risk with the highest reward.

Investing: We are leaving investing for last because it can be distracting for many. It is not just a distraction but can also help develop a coping mechanism. Something along the lines of: "By buying this, I will be able to take it easier and just sell it once it grows big enough." Everyone can do that, but it often leads to poor long-term performance. The reality is that if you do not have good cash flow (predictable + side business) and are putting significant amounts of money into it. Investing will not make you comfortable enough in the long run - your energy could be better spent elsewhere. Does that mean you should not invest? No. You should focus on the earlier aspects to get more out of it. If you cover all expenses, pay off your debt, fund your business, and still have some money left to invest. That money should be put in index funds (S&P500/QQQ) and big crypto coins (BTC/ETH). One could argue that it is risky enough to yield returns without being risky enough to go to zero.

Living Comfortably - Intermediate ($300K+)

Reality check: We argue that at least 30% of regular readers of our content fall into this category. A well-off position with multiple things going on. This is a solid position to be in, but at the same time, it's tricky. Why? Most get stuck in this range as the requirements to move things up become harder, or there is a missing piece of the puzzle. On top of that, add a feeling of comfort and the belief that you always have it- or at least that’s how most individuals think. Your mindset and approach should shift once you are over $300K in net worth (out of survival mode). Result of that shift? Understanding how to use your money on anything that positively impacts your life. ROI+ is one way to look at it.

Predictable income (W2-career): If you have played your cards correctly or followed our earlier advice. Your daily tasks should be automated. Meaning you are only spending your time on things that will move you forward and ensure you are in a better position. Extra points if you are already in a decision-making role that will make it harder for your employer to replace you. Results? More time to focus on what matters. The whole point of your work should be to put in the bare minimum necessary to get the most out - in case your goal is to 100% focus on building your business.

Side business: If you come to this point without having a side business, it just means you are wasting your talent and making someone else rich. Our advice? Put everything aside and focus on starting your business. Combine that with advice from above based on automation… Nothing left to add. A career loses its power because it has an earning cap that you will hit sooner or later. Over time, you will find yourself in a position where you have to give 110% to achieve what you could accomplish with much less effort in your business. The risk is different, and no one can deny it. But there is nothing to worry about if you have a system in place and never blindly went "all-in" as often preached online. Blind leading blind. The beauty of this approach is that once you find yourself with enough space to maneuver, starting the side business will become easier as your mind will stop finding excuses for why you can’t do it. Your goal? At least one additional income - still following the same principles as above. More income streams equal more freedom in the end.

Investing: Capital allocation and understanding the basics should be mandatory, as well as the power of compounding and what it means for your portfolio. Index investing vs. individual picks. Bonds vs. stocks. Crypto L1 vs. L2. What are treasury notes and all the rest of the good stuff? This article will not be about personal finances. We suggest you review Bankeronwheels material to pick up the basics if you have never had the time to do so. More so, considering where you are with your network. For the crypto basics, we would recommend checking out Crypto for Newbies. The main chunk of investment should be around crypto coins and index funds. If you understand what is happening and want to increase your risk exposure. Individual stocks will work and are worth looking into. The risk with individual stocks? Much higher compared to index funds. Crypto investing should follow a similar approach (BTC/ETH) and riskier options such as L2/L3. Another easy way to make more money than you have is by buying "stronger" alts at discounts (which happen often) and selling for 2x / 3x profits. Quite often, we do this and follow the same strategy. A great example of that would be DOGE before Trump won. Everyone knew how the market would react to Elon and Trump's partnership.

So many spend their health gaining wealth, and then have to spend their wealth to regain their health. - A.J. Materi

Health: On purpose, we are putting health in this article. Why? Because your health directly dictates how far you can push it. Basic example: you are in poor health and will need a certain sum of money to obtain the required procedures. Pretty self-explanatory. No one could argue that there is any risk associated with health. Also, this part should remind you never to let yourself go. No matter how much money you have. No matter what kind of side business you are running. No matter what corporate position you are chasing. Never put money before your health. Quite the opposite. Learn to invest in your health and find a way to perform better and make more money in the long run. This is something we plan to cover this year with a basic approach to how to spend your money on health.

Family: Another big factor when it comes to risk and health. If you are average or just above average in social skills, sooner or later, you will have a family (or at least there is a good chance). The difference? Huge. No kids = more risk. Kids = less risk. This applies to everything you can think of. Does that mean you should do something different? In terms of predictable income and side business? No. In terms of investing? Yes. You should gamble less (think meme coins or other risky bets) and focus more on vouched stuff (think S&P 500/BTC split). Safer investments are one way to put it. Another change you will need to introduce is related to living expenses. Following the same approach as before in this post, multiply the average monthly expenses by at least 6 months. Expenses and priorities are different when you have a family, and there is no reason to expose your family to unnecessary risks. It should be self-explanatory.

Impossible To Lose - Advance ($1.5mil+)

Reality check: Before anyone comments: "I know this guy. He had a few million, but he lost it all. So your impossible to lose category is nonsense". We also know a few of those brilliant minds and examples. But luckily for us… No one reading our material can relate to that. The reality is that it gets hard to lose after a certain point. Returning to zero is exceptionally hard - the risk factor goes way down. Money loves money.

Predictable income (W2-career): Hopefully, you are not in this position - golden handcuffs are real and should be avoided at all costs. If you are still working under someone else… You should rethink your choices. Time is the most valuable resource, and working for someone else with your money and backing is far from optimal. At this point, you should only work for yourself.

Side business: Very few cases exist of those who will manage to hit numbers like this (excluding inheritance) without having their equity (business). Suppose you are one of those who did so with their employment income through only their career. Congrats. But you did something wrong along the way. Multiple income streams? They should be in place, especially considering most can be run with a few clicks from your laptop. In this category, you should either have multiple smaller streams from your business or a single large business (brand) you are trying to scale. The options are limitless, and the more income streams you have, the better. Technically, it is the same approach you should use from the first category - just scaling it accordingly.

Investing: The only difference between this category and the previous ones is that you want to invest more money. Following the same principles as earlier. Willingly expose yourself more to ensure you beat guaranteed return types. This is where crypto will be your #1 investment vehicle to achieve that. What about the cash? Cash should never sit in your bank account. The only amount that should be in your bank account is the one you are not worried about getting hit with inflation and losing value over time. Your money should be working for you. Want to take risks down further but still beat the market? Treasury notes/bonds will take care of that. Your goal? Conclusion? More money in the risky positions you are not afraid of losing. Avoid leaving money useless - make it work for you.

Know what you own, and know why you own it. - Peter Lynch

Real estate: We said we won’t be touching real estate. However, this is where buying your property makes sense - when you have so much space and backing, going into debt makes sense. Especially when you consider that you can pay it off quickly. We are far from real estate experts, so take this with a grain of salt. Anything else before this amount? We would not recommend it if you are living in the first world. Real estate as investments? Not something we would recommend or do.

Scale: More cash flows. More income streams. More investments. More is the word you are looking for. Once you are set and have offset all the fundamentals (real estate, family, health), the only thing left to do is… Scale. Result? Sooner or later… you find yourself in a rarefied atmosphere. Playing the game with the big boys and drinking mid-day mimosas in your favorite country club.

Let’s Put It Into Practice - Scenarios

Three common scenarios that should further clarify risk management.

Scenario #1: Student debt, no investments, no income streams - fresh out of college - basic category. Risk-winning framework based on the scenario: Get a career → work on your savings → pay off the debt → focus on starting your business → pay off the debt → buy stocks/crypto. Results?

Scenario #2: No debt, investments split between S&P500 and BTC, high-paying career, no side business - impossible to lose category. Risk-winning framework based on the scenario: Focus on starting your business → buy a permanent location (if you plan to own one) → buy more stocks/crypto → focus on a business or start another one. Results? Out of golden handcuffs - multiple income streams and a bigger portfolio.

Scenario #3: No debt, no investments, no predictable income, multiple income streams (side business) - intermediate category. Risk-winning framework based on the scenario: Buy an initial chunk of stocks/crypto → save for a permanent location (if you plan to own one) → scale the business → buy more stock/crypto → scale the business

FAQ

Our risk management post is long and heavy with many dots to connect. Your best bet is to read it once or twice and refer to this FAQ. What you find here should put you in a good position with little to worry about. Every year, there will be progress, and things will get easier. Trust us on this. With this FAQ, we are wrapping up this article. If you feel lost or have specific questions - post them in the comment section.

Not in any particular order.

1) What is the most important factor in minimizing risk? Predictable income, side business, investments? Feeling lost… Not sure where to start.

Your primary focus should be business (equity), as it outperforms the others in how far you can push it. Got nothing going on? Predictable income - unsexy advice that works.

2) Underrated thing you can do to lower your risks?

Start taking care of your health asap. All the damage you do to your body will catch up as you age. Health directly affects risk and what you should do.

3) What crypto investments do you recommend?

This is something we plan to cover in the portfolio article, as explained earlier. BTC/ETH (boomer crypto split) will age well - you can’t go wrong with it.

4) Why would someone bother having a few months of expenses on the side when they could invest that money and make more? Doesn't having cash in a bank account defeat the whole point, as inflation is eating it?

Life can turn upside down in a matter of a week. Having at least 3 months of savings should allow you to care for your basic needs. It doesn't matter if you live with your parents, roommates, or alone… Calculate your average monthly expenses and multiply them by 3x.

5) When should one focus on investing, and when should one focus on paying off the debt? How do we prioritize one over the other?

It is subjective. The general rule should be that you are better off putting the money elsewhere if you beat the interest rate.

6) Am I considered wealthy/rich if I am in the "impossible to lose category"?

No. The wealth scale changes each year, and everyone reading this can see what has happened over the last few years in terms of prices and the true meaning of wealth. These categories are basic risk guidelines that should serve as good references. The reality is that it is hard not to make money if you have $1.5 million+ NW. We are not getting into the liquidity debate and what it truly means.

7) If you had to pick one thing off the list that would give the most results with the least effort. What should I focus on?

Company - pension fund match. It is free money and impossible to beat. Unfortunately, it is limited. Yet, it is a good starting point if you are in the first category.

8) What common mistake are those with a lot of money making because they fear risk?

Not using their money in the first place. Your money should be making you more money. Forget about leaving your money in the bank account. Your goal each year should be to beat 2% (Federal Reserve target)

9) When you say fund your business, does that mean I should prioritize it over other expenses?

No. But it means you should have zero excuses for not starting one. Most online businesses can be started for less than $150 - which you should have left at the end of each month in the worst-case scenario.

10) Should I still work for someone else if I am in the "impossible to lose" category?

Millions of examples exist of people still working for someone else with numbers such as those. Again, we are not saying they are impressive. The reality is that with a bit of creativity and effort… There is a good chance you will make more money working for yourself. Why? Sooner or later, there comes a moment when you realize that your time is better spent doing the opposite - working for someone else. Some individuals will understand this once they make their first $50, while others will take much more time.

11) Don’t you think these numbers are high?

Not even close. We could argue that these numbers are low, yet the concept remains the same. No individual in the first world with a high-paying career can't save $300K. There are cases, but it comes down to priorities and skill issues. If we remove those from the equation… Our numbers are realistic and low. The reality is that the number should look more like $300K→$600-750K and $1.5mil→$3-3.5mil. At least. On purpose, we didn’t use those numbers as we know that younger generations reading this will get discouraged. Yet, following the same principles and working toward those goals will undoubtedly land them in the "real categories." For those in the UK and Europe, these numbers are also becoming more relevant each year - those not from the "first world" will have to calculate their numbers based on their situation. There are too many specific cases for us to cover.

Disclaimer: None of this is to be legal or financial advice of any kind.

Easily the best letter going

As someone in the "1." Catagory this article was super helpful! Def gonna be coming back to this one quite a few times.

You convinced me to chill with the investments and start building up my actual savings. It's just hard to see money just sitting in an hysa account knowing it could be gaining more in some investment lol.